In 2010, Krugman had written an article captioned "The Austerity Myth". In the article, he basically laid out a case that austerity was a really bad idea in the midst of a recession. His opinion was that governments should expand in the midst of recessions and then move to austerity only after the recovery was well underway and the economy started to boom again. This is basic Keynesian economics. At the time, he was slammed by those on the right - remember the Tea Party was ascendant and Krugman seemed like a shrill and lonely voice.

As luck was have it, the world was about to witness the closest we've ever come to a controlled macro-economic experiment we can ever hope to achieve. Faced with virtually identical banking crises driven recessions, the US and EU chose very different paths. Obama and team pursuing a prescription that drew from the Keynesian formula. Meanwhile, Europe chose a path based on austerity. Given that the underlying crisis was the same and the economies were rather correlated before the crisis, this was sort of an experiment. So, how have we done?

Well, the short answer is that the two have diverged significantly.

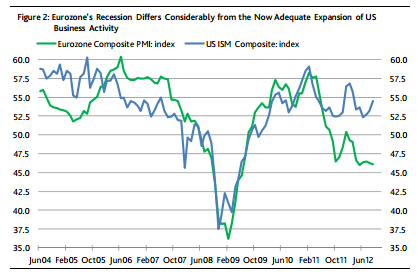

One article on the subject looked at economic activity using Moody's data:

As you can see, there has been a significant divergence between the two with the US growing, albeit slowly, while the EU is actually slipping back into recession.

Another article looks at stock performance. As the article explains: "Stock markets don't perfectly reflect underlying profit streams, but profits are certainly the key component to equity price sustainability."

Again, the US is growing, the EU is not.

And now we have a damning report by Oliver Blanchard and Daniel Leigh at the IMF which basically lays this bare. Here is their conclusion: "... Our results suggest that actual fiscal multipliers have been larger than forecasters assumed. ... We believe, however, that a reasonable case can be made that the multipliers used at the start of the crisis averaged about 0.5. ... actual multipliers were substantially above 1 early in the crisis."

Let me play this back in plain English. The actual negative effect of fiscal austerity, it turns out, was more than 2x what most economists prescribing austerity were assuming. In fact, a multiplier of >1 means that for every dollar in fiscal cut, the GDP shrank by an amount greater than the fiscal cut. Hmmm ... you know what, that sounds suspiciously like Krugman was right.

As luck was have it, the world was about to witness the closest we've ever come to a controlled macro-economic experiment we can ever hope to achieve. Faced with virtually identical banking crises driven recessions, the US and EU chose very different paths. Obama and team pursuing a prescription that drew from the Keynesian formula. Meanwhile, Europe chose a path based on austerity. Given that the underlying crisis was the same and the economies were rather correlated before the crisis, this was sort of an experiment. So, how have we done?

Well, the short answer is that the two have diverged significantly.

One article on the subject looked at economic activity using Moody's data:

As you can see, there has been a significant divergence between the two with the US growing, albeit slowly, while the EU is actually slipping back into recession.

Another article looks at stock performance. As the article explains: "Stock markets don't perfectly reflect underlying profit streams, but profits are certainly the key component to equity price sustainability."

Again, the US is growing, the EU is not.

And now we have a damning report by Oliver Blanchard and Daniel Leigh at the IMF which basically lays this bare. Here is their conclusion: "... Our results suggest that actual fiscal multipliers have been larger than forecasters assumed. ... We believe, however, that a reasonable case can be made that the multipliers used at the start of the crisis averaged about 0.5. ... actual multipliers were substantially above 1 early in the crisis."

Let me play this back in plain English. The actual negative effect of fiscal austerity, it turns out, was more than 2x what most economists prescribing austerity were assuming. In fact, a multiplier of >1 means that for every dollar in fiscal cut, the GDP shrank by an amount greater than the fiscal cut. Hmmm ... you know what, that sounds suspiciously like Krugman was right.

No comments:

Post a Comment